By Jackie, Researcher

Topic: Education

Area of discussion: Management and Cost Accounting

Chapter: Measuring relevant costs and revenues for decision-making

The primary objective of this posting is to critically describe the key concept that should be applied for presenting information for product-mix decisions when capacity constraints apply. In this discussion, I have taken a past year question from CIMA Cost Accounting 2 and prepared sample solutions with detailed workings to aid illustration purposes. Personally, I like this question because it is very tricky as ‘duo ranking system’ applies due to the nature of allotment and the presence of ‘market commitment’ in this question.

.JPG)

Suggested answers with workings:

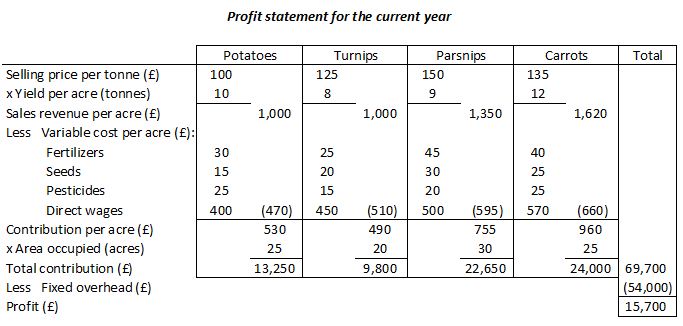

Solution for a(i):

Note: Variable costs are quoted per acre, but selling prices are quoted per tonne. Therefore, it is necessary to calculate the planned sales revenue per acre.

Solution for a(ii):

Ordinarily, the allocation of scarce resources will strictly follow the ascending order of rankings (in term of contribution amount); starting with the product that gives the highest contribution per limiting factor and then, leaving behind the balance of scarce resources to be taken up by other products that give lesser contribution per limiting factor. However, ‘market commitment’ exists in this case. So, the ‘market commitment’ will be the first one to get allocated. For profit maximization purposes, ‘market commitment’ has to be filled up with the product that gives the lowest contribution per limiting factor and the balancing figure to be taken up by other products that give a higher contribution per limiting factor. Also, due to the ‘market commitment’, the nature of allocation of scarce resource (i.e. land space) has been splitted into two.

Solution for b(i):

‘No market commitment and the land could be cultivated in such a way that any of the above crops could be produced’ simply means that the clause (i.e. the land that is being used for the production of carrots and parsnips can be used for either crop, but not for potatoes or turnips. The land being used for potatoes and turnips can be used for either crop, but not for carrots or parsnips. In order to provide an adequate market service, the gardener must produce each year at least 40 tonnes each of potatoes and turnips and 36 tonnes each of parsnips and carrots.) was not in effect anymore.

Solution for b(ii):

Note: To get 100 acres, sum up all the area occupied (i.e. 25 + 20 + 30 +25); while the contribution of £960/acre is taken from solution for a(i).

Solution for b(iii):

There are two ways to calculate this. The first one is to calculate the BEP in acres by dividing the fixed costs with the contribution per acre, and then used the computed figure to further multiply with its sales revenue per acre. (i.e £54,000 ÷ £960/acre = 56.25 acres, then 56.25 acres x £1,620/acre = £91,125). The second one is shown below by dividing the fixed costs with the contribution/sales ratio. Both methods are well explained in Cost-Volume-Profit analysis’ chapter.

Additional readings, related links and references:

Throughput accounting and TOC, one step beyond limiting factor analysis. The time frame is so short until all operating expenses are treated as fixed including direct labour; only direct materials are treated as variable. http://www.accaglobal.com/content/dam/acca/global/pdf/sa_nov11_throughput2.pdf

Reframing the Product Mix Problem using the Theory of Constraints

http://www.orsnz.org.nz/conf34/PDFs/Mabin.pdf

http://www.orsnz.org.nz/conf34/PDFs/Mabin.pdf

Product Mix: Determining My Winners and Losers

Limiting factors analysis

Short-term Decisions Overview and Product Mix Decisions

No comments:

Post a Comment